There are two types of investors in the world: the ones who say, “I’m fully invested,” and the ones who quietly say, “I’m ready.” In 2026, guess who’s sleeping better? Let’s talk about dry powder — the least sexy, most underrated financial move you’re probably not making enough of.

What is “dry powder”? (No, we are not talking about Milo powder)

“Dry powder” is just a fancy way of saying cash you’ve deliberately kept ready to use when opportunity strikes, not emergency money, and not “Oops I forgot to invest this.” It’s intentional, strategic, and slightly smug.

The term comes from old-school warfare (very dramatic), where you had to keep your gunpowder dry or… Well, things didn’t go well. In modern investing, the idea is simple: No dry powder = no ability to act when things get interesting.

Why dry powder is having a moment (again)

If 2020–2025 taught us anything, it’s this: 👉 Things get weird. Fast. And even Singapore — famously calm, collected, and CPF-organised — is thinking the same way.

The government has signalled it’s keeping financial “dry powder” ready in case global tensions escalate. So if an entire country is keeping cash ready “just in case', maybe your portfolio should too?

1. Markets are basically mood swings now

One week: “Markets rally!”

Next week: “Markets panic!”

Next next week: “Nobody knows why markets did anything.”

Having dry powder means:

- You can buy when prices drop (instead of texting your friends “should I sell???”)

- You’re not forced to panic-sell at the worst time

It’s the difference between: reacting vs being ready

2. Cash is no longer the boring kid - cash is king!

Remember when holding cash felt like punishment? “Congrats, you earned 0.05% interest 🎉” Not anymore.

In today’s rate environment:

- Your cash can actually earn something decent

- You’re getting paid… to wait

That’s like being paid to queue for bubble tea. Unheard of, but we’ll take it.

3. Opportunity doesn’t send calendar invites

The best financial opportunities are never like: “Hi, just checking if you’re free next Tuesday to make money?”

They show up as:

- Market dips

- Good deals

- Sudden ideas that might actually work

If all your money is locked up, your only options are:

- Miss it

- Or sell something else at a bad time

Neither feels great.

So, how much cash should you actually keep?

Let’s keep this simple and Singapore-practical.

Step 1: Don’t confuse this with your emergency fund

Emergency fund = “I lost my job” money/ I need money for medical emergency

Dry powder = “This is interesting 👀” money

Both important. Very different vibes.

📄 Read more about emergency fund

Step 2: Use a rough allocation

A good rule of thumb:

- Conservative: 20–30%

- Balanced: 10–20%

- Aggressive: 5–10%

In Singapore, where:

- Rent is high

- Life is seemingly more and more expensive every day

- And kopi somehow keeps getting pricier

It’s usually smart to lean slightly higher on liquidity.

Step 3: Adjust for real life

- Just started working → less cash, more growth

- Mid-career → more flexibility needed

- Planning big purchases → keep more dry powder

There’s no prize for being 100% invested at all times. (There is regret though.)

The real problem: Having zero dry powder

Here’s what nobody talks about: Being fully invested sounds smart, until it isn’t.

Without dry powder:

- You miss buying opportunities

- You feel stuck during market drops

- You make rushed decisions

Meanwhile, the person with cash is just sitting there like: “Interesting… I might buy.”

Top vehicles for holding dry powder in Singapore

You don’t want your cash just sitting there doing nothing.

You want it:

✔ Accessible

✔ Earning something

✔ Not costing you fees

Here’s what most Singapore-based investors are using to park their spare cash right now: Read more about the best rate for your money in Singapore

1. Cash Management Accounts

- Daily liquidity

- Competitive rates

- No lock-ins

The “main character” of dry powder.

📄 Check out our low down on popular Singapore Cash managed accounts: Chocolate Finance Vs Stashaway Vs Syfe Vs Endowus

📄 Read more about cash management accounts

2. Money market funds

- Low risk

- Slightly better returns

- Still liquid

Who this is for: people who want a bit more optimisation

3. Fixed Deposits (Short-Term)

- Predictable returns

- Less flexible

Good for some of your cash, not all

📄 Read more about fixed deposits (Short-Term)

4. Singapore T-Bills

- Government-backed

- Low risk

- Fixed duration

For structured, short-term parking

📄 Read more about Singapore T-Bills

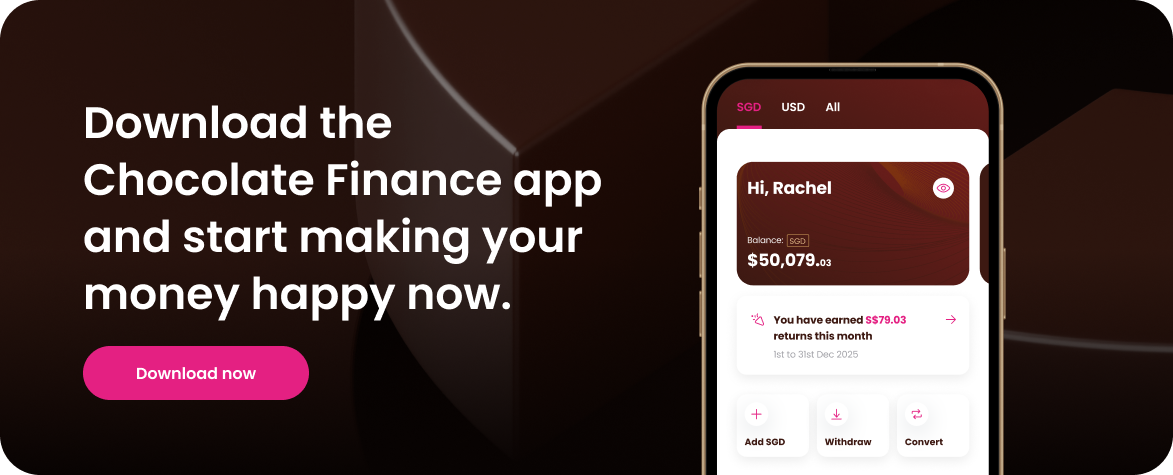

Where Chocolate Finance comes in

Let’s be honest. The goal isn’t to hoard cash like a dragon. It’s to keep your money ready — while it still works for you.

Here’s what you can look forward to with Chocolate Finance:

- Cash can earn - like 2% p.a. On your first S$20k and 1.8% p.a on your next S$80k.

- Liquidity is powerful - Withdraw anytime, Most withdrawals are completed within 36 hours.

- Flexibility is underrated - no hoops, no lock ins, no fees

The smartest investors aren’t just chasing returns. They’re building optionality.

Final thought: The quiet advantage

Most people optimise for: “Am I fully invested?” The better question is: “Am I ready?” Because when the right opportunity comes, you won’t have time to rearrange your finances.

You’ll either have dry powder… Or you’ll have a story about how you almost did something smart. And honestly, we have enough of those already.

Disclaimer

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)