Lowering interest rates means fixed deposits are losing their lustre. Here’s why that’s happening, and some alternative ways to grow your money.

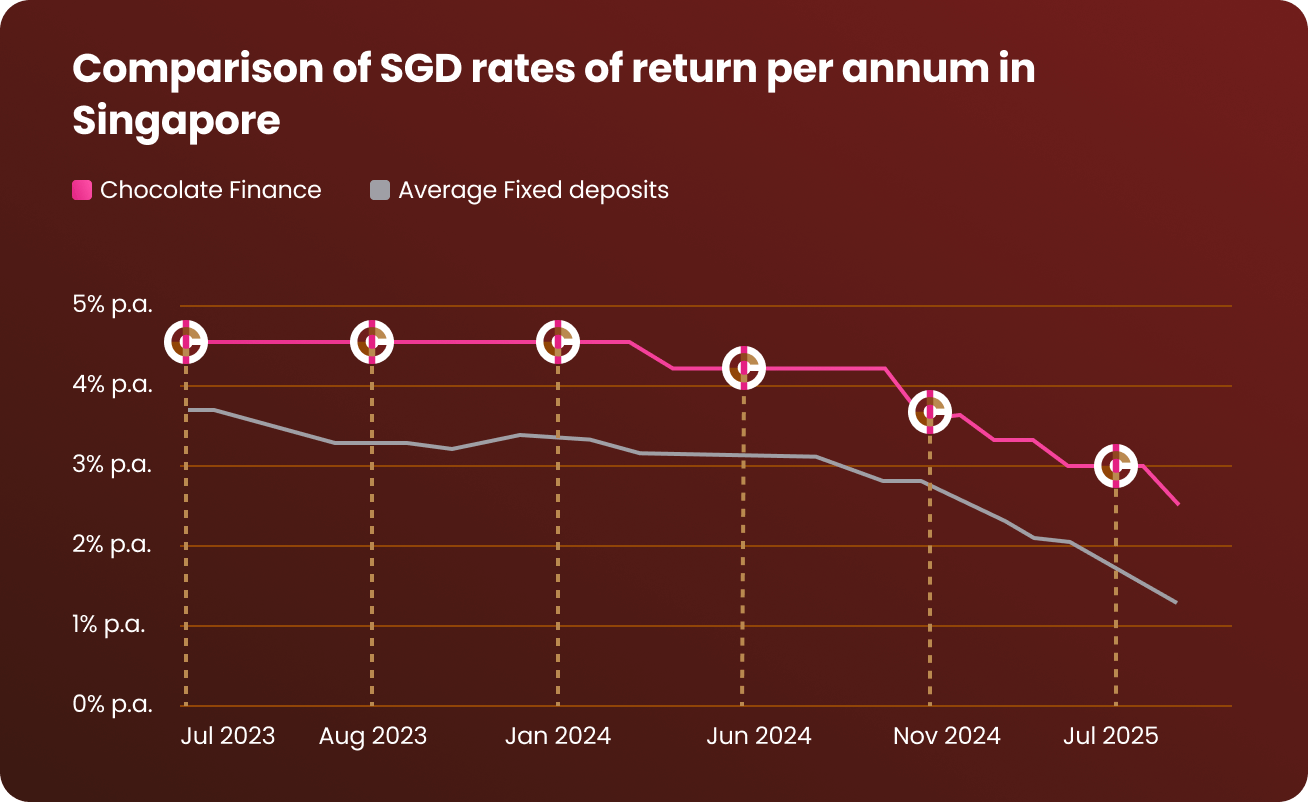

Fixed deposit rates in Singapore continue their downward slide, with 12-month rates topping out at 2.45% p.a. as of September 2025 – a far cry from the glory days of around 4% p.a. returns, last seen in 2023.

Source: Fixed deposit rates retrieved from official bank websites and public disclosures. Data accurate as of September 2025. Banks included: Bank of China (3 mth), CIMB (3 mth), Citi, DBS (9 mth), Hong Leong Finance (9 mth), HSBC, ICBC (3 mth), Maybank (12 mth), OCBC (9 mth), RHB (12 mth), SBI (6 mth), Sing Investment & Finance, Standard Chartered (5 mth), UOB (6 mth).

Low fixed deposit rates means depositors are getting less-than-optimal returns, which impact financial goals especially over the long run. Fixed deposits are attractive because they offer risk-free returns, but this value proposition dwindles as interest rates fall. And in the face of alternative solutions that offer higher returns with a similarly low risk profile, isn’t it time you reconsider your approach to growing your money?

Why are fixed deposit rates falling?

Fixed deposit rates are influenced by a series of macroeconomic factors, chiefly interest rate policies by central banks, especially the U.S. Federal Reserve (aka the Fed).

In early 2025, Trump launched trade tariffs which caught the market by surprise. This further increased market uncertainty and worsened the global economic outlook. As a result, there is greater expectation for the Fed to cut interest rates, a move which will likely be followed by other central banks around the world.

Given that a lower interest rate environment is expected, banks are making adjustments to fall in line with prevailing conditions. One such change is the lowering of fixed deposit rates, which help banks better manage funding costs.

This change applies to banks in Singapore too. This is because the Singapore Dollar is managed against a trade-weighted basket of currencies, with heavy influence from the USD. This means Singapore interest rates tend to move in tandem with US rates.

Furthermore, Singapore’s open capital flows necessitate that local interest rate does not stray too far from those of global rates.

These factors cause local banks to adjust fixed deposit rates in line with overall economic expectations.

How about alternatives to fixed deposits?

With fixed deposits becoming less attractive, where else can you park your money for optimal returns? Are interest rate cuts by the Fed affecting only fixed deposits?

To answer these questions, let’s take a look at some alternative solutions.

High-yield savings accounts

High-yield savings accounts offer higher interest rates on deposits, but only if you fulfil several conditions. Some of these include maintaining a minimum balance; crediting your salary; spending a minimum monthly amount on a credit card; purchasing an insurance plan from the bank, and making a certain amount of investments.

That’s a lot, but those willing to jump through all those hoops can enjoy interest rates ranging from up to 4.5% p.a. to up to 8.05% p.a – this varies according to which bank account you choose.

And yes, high-yield savings accounts have been affected by falling interest rates too. Several banks in Singapore have already reduced rates, or are set to do so.

Treasury Bills (T‑Bills) & Singapore Savings Bonds (SSBs)

Another popular instrument for risk-free returns are Singapore Savings Bonds (SSBs) and MAS Treasury Bills (T-bills). These are backed by the Singapore government and provide a fixed return to investors, known as the yield.

SSBs and T-bills have not been spared from falling interest rates, leading to declining yields.

For SSBs, the latest issuance in June 2025 offers an average yield of 2.49% p.a. over 10 years. This is markedly lower than the 10-year average rate of 2.86% p.a. seen in January.

Meanwhile T-bills are seeing a similar decline. The latest six-month T-bill saw cut-off yields fall from 2% p.a. to 1.44% p.a. This marks the lowest level of yield this year, and the eighth consecutive issuance for which yields have declined.

Given the current trend of declining yields, T-bills and SSBs may no longer stand as attractive alternatives to bank fixed deposits for those seeking to grow their cash.

Flexible managed accounts like Chocolate Finance

Managed accounts can offer similar – or even higher – returns to fixed deposits, but it’s important to understand how they work.

Firstly, managed accounts are not the same as a bank account, which means your account balance is not protected by SDIC – but there are other protections put in place in accordance with MAS requirements.

Secondly, managed accounts are managed by professional fund managers that seek to outperform prevailing interest rates returns, while minimising market risk. This is why managed accounts can be a viable alternative to fixed deposits and other risk-free instruments.

What Chocolate Finance can do for your money

It’s important to realise that not all managed accounts are made the same.

Chocolate Finance offers up to 2.5% p.a. on your SGD balance, and up to 4% p.a. on your USD balance.

And let’s not forget the Chocolate Top-Up Programme, which locks in your returns on the first $50,000 in your SGD and USD balances. At the time of writing, the Top-up Programme will be in effect until 31st December 2025, or until the assets under management for the Chocolate Managed Account reach S$1 billion – whichever comes first. (Chocolate Finance reserves the right to extend or remove the programme at its sole discretion).

But that’s not all! Earn frequent flyer miles when you spend on the Chocolate VISA Debit Card to enjoy air travel perks. Every S$1 spent earns 1 Max Mile, up to S$1,000 each month. Thereafter, you’ll earn 0.4 miles per dollar. Bill payments earn Max Miles too, capped at 100 miles per month.

See? Managed accounts are not made the same. Chocolate Finance lets you continue enjoying high returns even when interest rates are low, and earn miles for your next global adventure as you spend. Sign up and make your money happy today.

Key takeaways

- Expect a prolonged low‑rate cycle. Forward‑rate markets price two more 25 bp Fed rate cuts by December 2025.

- Blend your cash strategy. Consider allocating across a HYSA for day‑to‑day liquidity, T‑Bills/SSBs for sovereign safety, and a managed account like Chocolate for higher returns.

- Review quarterly. Promotional tiers, returns and yields can change without notice.

Disclaimer:

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)