Savings accounts, money market funds or cash management accounts? Choosing the right one depends on what needs you’re trying to meet. Here’s how to decide.

If there’s one good thing we can take from the unwelcome trend of climbing prices, it’s this: The negative effect of inflation is becoming visible in everyday life. Just imagine what will happen to your future ability to afford things if prices continue to run rampant over the next five, 10 or 20 years.

The solution isn’t simply to save harder – although that helps to a degree. Instead, we need a smarter approach to how we are managing our cash. The goal isn’t just to beat inflation (thereby preserving your purchasing power); but to do so in a way that doesn’t crimp your access to your savings.

Why being deliberate with cash management matters in Singapore

We all know that inflation hits especially hard in Singapore, one of the most expensive cities in the world. With every bill draining your money, what matters isn’t how much you save, but how accessible your money is when you need it.

As Chocolate Finance’s CEO, Walter de Oude, puts it, “Financial stress may not come from one big bill. It builds when you have lots and lots of small bills that stack.”

Being deliberate about your cash is the key. Paying attention to returns alone won’t cut it. Instead, savers need to consider liquidity, flexibility and peace of mind – an approach that requires expanding your options.

Savings accounts, money market funds, or cash management accounts?

Here’s the truth: Relying on just a savings account alone doesn’t give you a well-rounded strategy for managing your cash savings. Money market funds and cash management accounts can add flexibility and boost returns – but there are important caveats involved.

Before we get into the nitty gritty, let’s first take a look at how the three stack up.

At-a-glance: savings accounts vs money market funds vs cash management accounts

Savings accounts: Best for daily spending, cash you need immediately

For savings accounts, it’s pretty much a case of “what you see is what you get”. Interest is lowest of the three (at least for basic accounts) and unlocking higher interest will require completing additional bank transactions. These may include salary crediting, credit card spends, maintaining or increasing your account balance, purchasing insurance, making investments and taking up other bank products.

The main drawback of savings accounts is that earning higher interest takes a bit of work and planning. Failing to complete the required actions will leave you with interest so low it doesn't even cover nominal inflation.

For this reason, savings accounts aren’t the best choice for keeping your savings over prolonged periods if you’re unable or unwilling to keep up with the requirements for higher interest. Your savings are being eroded over time, and the longer you keep them in a basic savings account, the worse it gets.

Money market funds: Better returns, but requires longer holding periods

On the other end of the spectrum, money market funds can offer significantly higher returns than basic savings accounts, but require some understanding and finesse in handling.

The money put in a money market fund is pooled together and invested in a variety of short-term, high quality investments such as debt securities, cash and cash equivalents. Investment returns are not guaranteed, and account values fluctuate according to market volatility.

As money market funds come with higher volatility – account values fluctuate according to market conditions – withdrawals must be timed with care. If you find yourself needing access to your cash during a market dip, you’ll be caught in an unfavorable position.

As such, money market funds are better used for medium- to longer-term savings. Being able to hold your cash longer improves your account’s ability to ride out the volatility and achieve better returns.

Cash management accounts: Higher returns with flexibility

So far, we’ve seen that basic savings accounts aren’t great for returns, while money market funds require a bit more care.

Cash management accounts sit somewhere between the two – providing you with higher returns and greater flexibility for withdrawals. The four most popular cash management accounts in Singapore are Chocolate Finance, Syfe Cash Plus Flexi, StashAway Simple, and Endowus Cash Smart Secure.

All of them are MAS-licensed, and they provide higher returns than typical savings accounts without lock-ins. As these platforms differ in projected returns, fees, withdrawal speed and features, you can compare these four options to help you choose the best one for you.

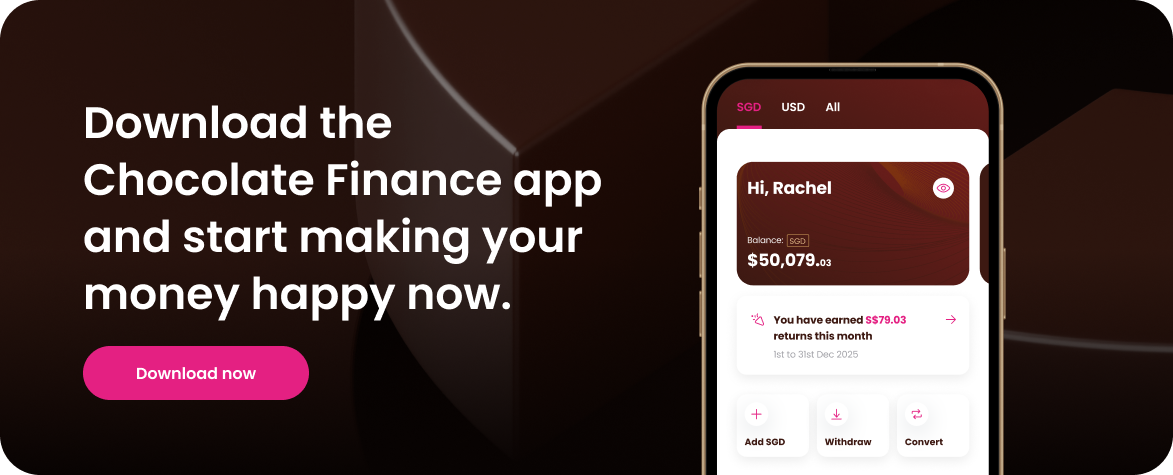

With Chocolate Finance, you can keep cash accessible – withdrawals are typically processed on the same day or by the next – while earning meaningful returns that actually gives you a chance to keep pace with inflation.

As Walter sums it up, “Imagine returns, without hoops or lock-ins where you can take your money out at any time.”

Another advantage? There are no monthly charges to pay, and no fees are taken until stated returns are delivered. And here’s what’s truly unique to Chocolate. The first $20,000 in both your SGD and USD balances are covered by Chocolate’s Top-Up Programme – meaning you’ll receive the stated returns of 2% p.a. (SGD) and 4.1% p.a. (USD) respectively.

A layered approach to smarter money management

So out of savings accounts, money market funds, and cash management accounts, which one should you use?

Well, you don’t have to choose just one. In fact, depending on your needs, habits and priorities, a layered approach might prove the most optimal.

Savings accounts

Maintain a bank account for everyday spends and buffer cash to use when unexpected expenses crop up. Try to keep this amount small to limit loss of purchasing power.

Cash management accounts

Use this to store savings meant for short-term goals, such as travel or lifestyle purchases. The higher returns will help you grow your savings too.

Money market funds

This is where you can put money you do not need to use in the medium- to long-term (from a few months to several years). As there’s lesser urgency, your funds have more resilience to ride out market volatility and optimise returns.

Happy money starts with Chocolate Finance. Enjoy up to 2% p.a. on your first S$20k, up to 4.1% p.a. on your first US$20k, and earn HeyMax miles when you spend with the Chocolate VISA Debit Card – all with zero fees or subscriptions! Sign up now.

Disclaimer

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)