If you've spent any time on popular reddit communities like r/singaporefi lately, you already know the debate. It shows up every single week in some form: "Would it be wise to continue to DCA?" "DCA or lump sum?" "Is it still worth it to DCA into S&P 500?" "How much to DCA?"

The reddit community is split. But both sides are making the same mistake.

On one side, you've got the disciplined DCA (dollar cost averaging) crowd — the ones putting $500 or $1,000 into VWRA (Vanguard FTSE All-World UCITS ETF) every month like clockwork, rain or shine. Posts like "DCA monthly into VWRA and nothing else — pretty decent performance" sit at 200 upvotes. A 30-year-old earning $2k–$2.5k a month asked "how to DCA?" and got over 400 upvotes and 158 comments. The message is clear: just start, stay consistent, don't overthink it.

On the other side, you've got the people sitting on cash, waiting. Waiting for a correction. Waiting for clarity on interest rates. Waiting for the market to "make sense" again. They're not wrong to be cautious — but they're not deploying either.

Here's the thing both sides have in common: cash sitting in between.

The DCA investor has money waiting for next month's buy. The cautious investor has money waiting for the right moment. And in both cases, that cash is almost certainly parked in a savings account earning next to nothing.

The real cost of idle cash

Let's be honest about what "waiting" actually costs you in Singapore right now.

Most bank savings accounts offer well under 1% p.a. unless you jump through hoops — salary crediting, card spending minimums, bill payments, insurance purchases. Miss one criterion and your rate drops to the base: often 0.05% p.a. On $20,000, that's $10 a year.

Fixed deposits are slightly better, but they lock your money up. If you're DCA-ing monthly, you can't have your cash tied to a 6-month tenure. And if you're waiting for the right entry point, locking up defeats the whole purpose — you need to be ready to move.

Meanwhile, inflation quietly chips away at your purchasing power. Your cash isn't just sitting still. It's going backwards.

Whether you're investing $1,000 on the 1st of every month or sitting on $30,000 waiting for a pullback, the question is the same: why is that money not earning anything while it waits?

The DCA investor's problem

You've got the strategy nailed. VWRA, IBKR (Interactive Brokers.), monthly contributions, long time horizon. The r/singaporefi starter pack. Brilliant.

But between each contribution, there's a gap. Salary lands on the 25th. Your buy goes through on the 1st. That's a week of dead money. And if you're one of the many Redditors who batches their DCA quarterly to save on brokerage fees — threads like "any potential downside to DCA large amount into IBKR?" suggest plenty of people do — that's potentially months of cash earning nothing.

Your emergency fund sits idle too. The $15,000–$25,000 most Singaporeans are advised to keep liquid? In a standard savings account, it's barely keeping up with the interest on your HDB loan.

The "waiting for the right moment" investor's problem

You've done the research. You know the market looks stretched. You've got a target entry point in mind, or you're waiting for earnings season, or you want to see how the next Fed meeting plays out.

All perfectly reasonable.

But while you wait — and waiting can last weeks, months, sometimes longer — your entire war chest is earning almost nothing. Every day that passes is a day your cash could have been generating returns. And when the opportunity finally arrives, you'll deploy from a pile that's been slowly losing value to inflation rather than one that's been quietly growing.

The irony? Being cautious with your investments while being careless with your cash.

What both sides need is the same thing

Whether you invest like clockwork or wait for your moment, the requirement is identical: a place where your cash earns returns and stays fully accessible at a moment's notice.

Not locked in a fixed deposit. Not tied up in conditions. Not earning 0.05% because you forgot to hit your card spending target.

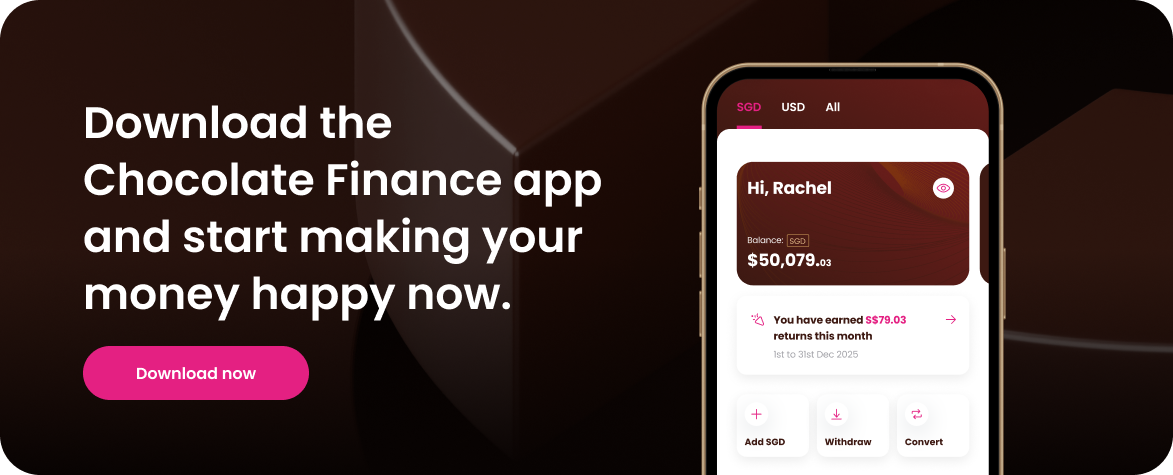

This is exactly what Chocolate Finance is built for.

Daily returns from the very next day. Your money starts earning the moment you add it. Not at the end of the month. Not after meeting criteria. Every single day. Whether your cash is here for a week between DCA contributions or three months while you wait for the right entry point — it's working.

Withdraw whenever you're ready to move. No lock-ins, no penalties, no maturity dates. When your DCA date comes around, withdraw and buy. When the dip you've been waiting for finally arrives, your cash is there — and most withdrawals are processed within 24 hours. Chocolate never gets in the way of your strategy.

No conditions, no fine print. No minimum balance. No salary crediting requirement. No card spending hurdles. Your returns don't depend on jumping through hoops. They depend on one thing: having money in your account.

Set it up once and forget about it. Schedule automatic top-ups via eGIRO — weekly, monthly, or quarterly — and your cash flows into Chocolate without you thinking about it. One less thing to manage while you focus on your actual investment decisions.

Two investors, one solution

The DCA investor: Salary → auto-top-up to Chocolate → cash earns daily returns → withdraw when you want → buy VWRA → repeat. Every dollar earns something, even if it's only there for a few days.

The opportunistic investor: Bonus / savings → park in Chocolate → cash earns daily returns while you research, watch, and wait → the moment arrives → withdraw and deploy. Your war chest grew while you were being patient.

Different strategies, same outcome: no idle cash.

Your strategy is your business. Your cash is ours.

We're not here to tell you whether to DCA or time the market. That debate has been raging on Reddit since the beginning of Reddit, and it'll keep going long after this post. Both approaches have merit. Both have trade-offs. That's for you to decide.

What we will say is this: whichever side of the debate you're on, there's no good reason for your uninvested cash to be earning nothing.

The market will do what the market does. In the meantime, make sure your money is doing something too.

Disclaimer:

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)