High-yield savings accounts offer good rates, but require jumping through several hoops. Is there a better way to earn increased returns?

According to a recent Straits Times report, younger Singaporeans have a strong preference for high-yield savings accounts (HYSA). The report noted that savers aged 18 to 30 are drawn to the risk-free returns offered by such accounts, with higher rates progressively unlocked as different conditions are fulfilled.

It’s easy to see the appeal. HYSAs promise interest rates several times higher than the base rate, providing an opportunity to grow your savings quicker or generate some extra cash. However, are Singaporeans really getting a good deal from HYSAs, and is there a better way to earn better returns on your money?

HYSAs: Here’s how they really work

At first glance HYSAs offer attractive propositions. Such bank accounts promise to pay out interest on your deposits ranging from around 3% p.a. to as high as 8% p.a. That’s on par with Singapore Savings Bonds, and even beating the S&P 500 in some years.

But before you rush to sign up, here’s the truth about how such accounts really work. HYSAs offer ramp-up interest rates that increase as you fulfil the required banking transactions. In other words, there are conditions you have to fulfil – and ongoing ones at that – before you can enjoy higher returns on your deposits.

If you fail to meet or maintain the required transactions, you will not earn the advertised interest rate. Instead you’ll earn a lower interest rate according to the banking requirements you do happen to meet.

This wouldn’t be that bad if getting to the highest interest rate was easy; unfortunately, it’s not. Just to give you an idea, to enjoy the highest rate provided by a HYSA, you may have to:

- Credit your salary monthly

- Spend a minimum amount on a credit card per month

- Make certain transactions per month

- Maintain a specified minimum or average balance

- Save a required amount

- Purchase an insurance plan

- Purchase investment products

And to make things more complicated, most HYSAs pay bonus interest up to a certain amount in your bank balance – typically S$100,000. Any amount beyond that only earns the base interest rate.

What earning higher returns from HSYAs really looks like

Let’s take a look at three popular HYSAs and the steps you have to take to earn higher returns on your savings. The information presented below is derived from publicly available sources, and accurate as at Sep 2025.

Here are a couple of things to note about these HYSAs. Bonus interest for invest and insure transactions are paid for a limited duration, ranging from 6 months to 1 year. To continue earning bonus interest you’ll need to make another investment or purchase another insurance plan.

Some requirements are also out of reach for many young Singaporeans. For instance, two of the requirements in Citi Wealth First Account are to take a mortgage of at least S$500,000, and to increase your account balance by saving at least S$3,000 every month.

Speaking of high requirements, the UOB One Account offers up to 4.5% p.a. interest, but only if your bank balance is between. S$125,000 and up to S$150,000 (and you fulfil the qualifying transactions). If your bank balance is S$75,000 or lower, the maximum interest you can earn is 1.5% p.a., and 3% p.a. for account balances over S$75,000 and up to S$125.000.

The bottomline? Young Singaporeans may love HYSAs, but it appears the affair is rather one-sided. The truth is HYSAs are targeted at higher earning individuals looking for better returns on six-figure bank balances,

Unfortunately this does not fit the majority of younger Singaporeans who realistically only receive a fraction of the advertised, due not meeting or qualifying for all the required conditions.

If you’re wondering whether your HYSA is performing up to expectations, use this online calculator to check it out. You can model what are the returns you’re likely to get based on your estimated transaction amounts.

Are there better options for returns than traditional savings accounts?

Right, so we’ve seen that earning the maximum interest dangled by HYSAs is no easy feat. Is there an easier way to get higher returns on your money?

We’re glad you asked! Cash managed accounts invest your cash in low-risk assets and investments to generate higher returns than traditional bank accounts. Some of these investments include short-term debt instruments such as money market funds and short-term bond funds, ensuring liquidity while reducing risk.

As such, cash managed accounts are quickly gaining traction as an alternative to bank savings accounts, due to their ability to generate higher returns while maintaining the freedom for users to withdraw their funds anytime they wish.

But it’s important to understand that cash managed accounts are not bank savings accounts, and are therefore subject to market risk – even if the risk remains low due to the nature of the underlying investments. Another thing to note is that cash managed accounts are not covered by SDIC, but that isn't necessarily a problem, as we’ve explained here.

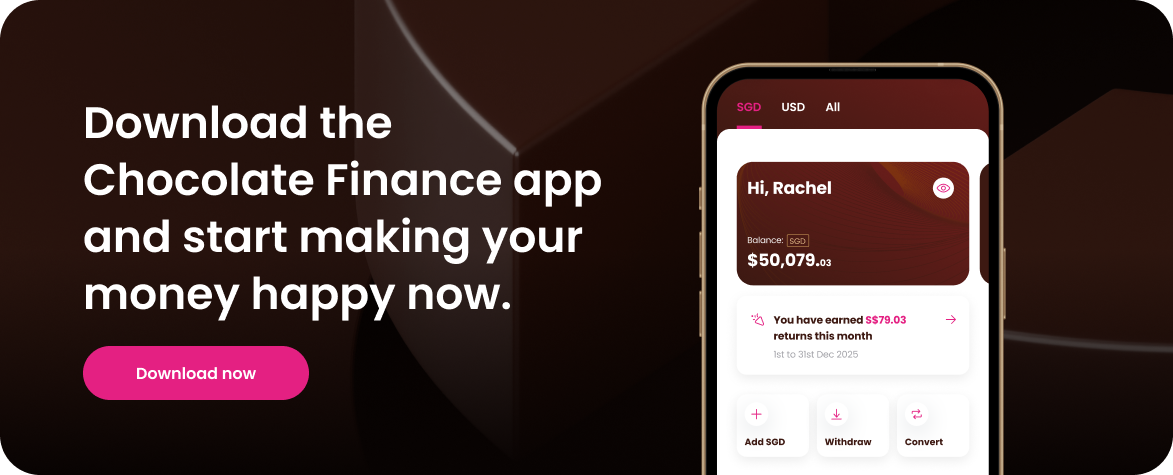

Chocolate Finance is a cash managed account that helps you with happy money by making it easy to earn returns – no hoops, no complicated tiers, no high barriers to entry.

In fact, with Chocolate, there’re no hoops! Simply add money and start earning happy returns that you can see daily in your mobile app. Here’s how much returns you can enjoy:

The Chocolate Finance Top-Up Programme also supports your first S$50k and US$50k - where if the returns for your first S$50k (2.5% p.a. on your first S$20k and 2.2% p.a. on your next S$30k) are not met, then, the difference will be topped up during the qualifying period. Learn more

Other features you’ll love

SGD, USD or both!

See that column marked “USD”? Yep, Chocolate offers SGD and USD balances, so you can diversify your funds across two different currencies. (Or simply stay with one, it’s your money!)

This gives you the option to enjoy higher returns of up to 4.3% p.a. by converting some of your money to USD – handy if you’re waiting for opportunities in the US stock market, or saving for a trip to the U.S.A.

Earn HeyMax miles as you spend

Speaking of travelling, did you know that the Chocolate VISA Debit Card offers zero FX fees? That means you’ll enjoy better savings on overseas transactions.

But that’s not all. Spend with the Chocolate VISA Debit card and earn one HeyMax mile per dollar. Max Miles can be redeemed for flights at a fixed rate, or exchanged 1:1 for points at 28 airline and hotel loyalty programmes – that means you could enjoy free flights or hotel stays the next time you travel!

Happy returns with Chocolate

With Chocolate, you’ll enjoy happy returns without having to jump through multiple hoops, or constantly watching your balance lest you fall below. We make it easy and fuss-free to earn happy returns on your money because we believe that’s just how things should be.

And with no lock-ins, the freedom to withdraw at any time, and daily returns you can see on the app, you’ll maintain complete control over your money in every way that matters.

So if the rigorous requirements of HYSAs are getting you down, don’t fret. Choose happy returns instead with Chocolate.

Disclaimer:

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)