Most people think financial security comes down to one thing: Save more, spend less. But as costs rise across Singapore, that advice is starting to fall apart.

On the Business Times Money Hacks podcast, Walter de Oude, founder and CEO of Chocolate Finance, explains why:

“Life is not a straight line… if everything was in a straight line, having a good budget can manage you. But if the line is moving, we have to be more prepared than just having a budget.”

And right now, that line is moving fast.

Why budgeting alone doesn’t protect you anymore

Inflation doesn’t hit all at once. It creeps in. Petrol goes up. Groceries increase. Electricity ticks higher. Transport costs rise.

Individually, manageable. Together, overwhelming.

“Financial stress doesn’t always come from one big bill… it comes when you have lots and lots of small bills that all stack.” Walter de Oude, Business Times, Money Hacks Podcast, 1st June 2026

This is the new reality: financial stress is no longer about shocks — it’s about accumulation.

The mistake most people make with emergency funds

Many people think: “I have savings, so I’m covered.” But that’s not the same as being prepared. Putting it away doesn’t always necessarily mean that you are financially prepared for a liquid event. The real question is:

- Can you access your money immediately?

- And what happens when you do?

The important question you need to ask yourself is :

“If you had that money put away… can you access that savings when you need to? And will there be a financial consequence if you access it?”

Money in:

- Fixed deposits

- Insurance policies

- Long-term investments

- Locked-up or illiquid financial products

…might look like savings but it’s not liquid.

What liquidity actually means (and why it matters)

Liquidity is simple: Cash you can access immediately, without penalties.

And more importantly having readily available cash… is actually really good at reducing financial stress. This is the real goal of an emergency fund:

- Not just to exist

- But to be usable at the exact moment you need it

How much emergency fund do you really need?

Walter’s emergency fund rule is straightforward:

“Somewhere between 3 and 6 months of salary or 6 months of expected expenditure is the right amount.” Walter de Oude, Business Times Money Hacks podcast, 1st June 2026

But context matters:

- Stable job → ~3 months

- Single income household → 4–6 months

- Freelance / variable income → 6+ months

Or more simply:

“Having 6 months of your future expenses readily available in cash is a minimum… for helping you sleep better at night.”

Where should you keep your emergency fund?

This is where most people get it wrong. Traditional savings accounts are:

- Safe

- Accessible

- But earn almost nothing

“You can put it in a traditional bank account… but it’s going to give you next to no interest at all.”

On the other hand:

- Fixed deposits → better returns, less flexibility

- Investments → higher risk, wrong timing

So the real challenge becomes: how do you keep cash accessible and earning something?

The middle ground: cash that works for you

“What you want to do is have it readily available and earning the best returns you possibly can.” Walter de Oude.

This is where newer solutions like cash management accounts come in.

They aim to:

- Keep your money liquid

- While improving returns vs traditional savings

As Walter explains:

“Imagine returns better than a fixed deposit, but you could take it out anytime.”

That’s exactly the problem Chocolate Finance was built to solve — helping people get better returns on short-term cash without locking it away.

The real goal: reduce financial stress

At the end of the day, this isn’t about optimisation. It’s about peace of mind.

Because what people actually want isn’t a perfect budget — it’s certainty.

“What you really want to do is be able to sleep at night knowing that you can weather that storm… and you don’t have to tap into your long-term savings unnecessarily, and at a cost.” Walter de Oude.

Final takeaway

An emergency fund isn’t just about how much you save.

It’s about:

- How accessible it is

- How fast you can use it

- And whether it actually protects you in real life

Because in today’s environment, liquidity isn’t a nice-to-have

It’s the difference between:

- Looking financially stable

- And actually being prepared

The fear of getting started is real. Change is difficult, and the fear of the unknown often makes money feel overwhelming — so much so that doing anything about it feels hard. Most people end up sticking their head in the sand, knowingly or unknowingly falling into the same pattern.

That’s where simplicity matters. Chocolate Finance is designed to help people overcome that inertia — offering a straightforward place for your spare cash to sit, earn consistently competitive returns, and remain accessible when you need it, without penalties.

Read more about Liquidity: the anxiety antidote here.

Disclaimer

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

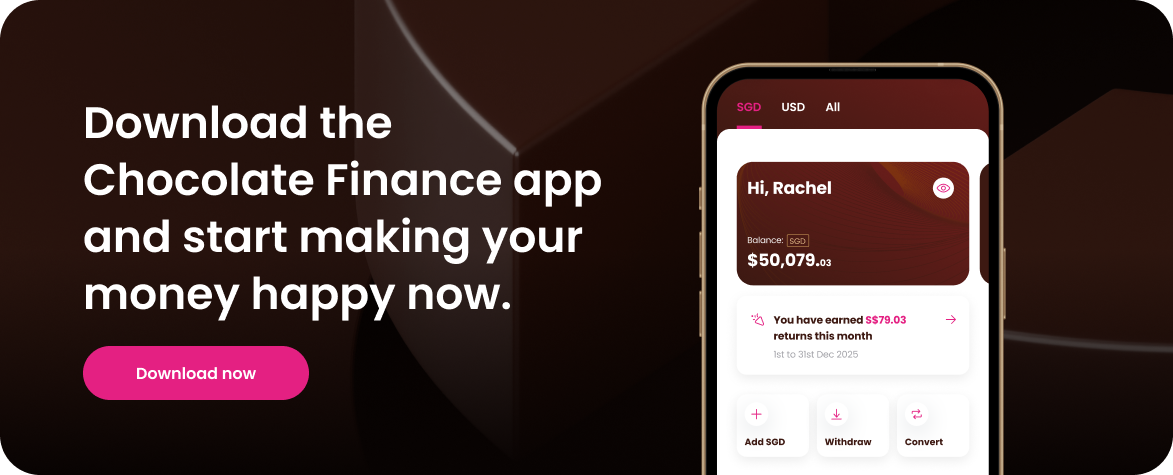

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)