From returns rate to underlying funds, here’s everything you need to know about cash management accounts in Singapore, and how to choose the best one for your spare cash.

Cash management accounts stand as a great alternative for those who want to get better returns on their cash savings without having to go through lock-in periods. Highly convenient, they work similarly to a bank account, allowing you to top up and withdraw your cash anytime you wish.

The key difference is that cash management accounts often offer higher returns than your ordinary bank account base rate– you could be getting around 2% p.a. with the former, compared to a base rate of 0.05% p.a. for the latter.

Curious whether management accounts like Chocolate are right for you? You’ve come to the right place. Strap in as we dive under the hood of cash management accounts to see what makes them tick, learn their distinct differences, and discuss the benefits they provide.

Cash management accounts explained simply

Are cash management accounts savings accounts?

No, cash management accounts and bank savings accounts are two different things altogether, although they offer overlapping functions. Both act as a convenient, flexible way to store your cash and grow your cash savings, but that’s where the similarities end.

Bank saving accounts

A bank savings account is where you can deposit your cash for safekeeping with the bank. In return you’ll receive interest on your savings, which is typically paid every month. By default you’ll receive the base interest rate, but you can earn a higher rate by fulfilling additional requirements, such as

- Purchasing an insurance policy,

- Making a certain number of transactions,

- Spending a stipulated amount on your credit card

Also, savings in banks are covered by SDIC which protects Singapore dollar deposits up to S$100,000 per depositor per member bank if a bank fails – investment products like cash managed accounts are not covered by this.

Cash Management Accounts

In contrast, a cash management account invests your cash into the market to generate returns. Only specific market instruments are chosen in order to keep risk low (more on this later).

This difference is how cash management accounts are able to give you happier returns compared to bank savings accounts. You can directly benefit from prevailing market conditions without having to jump through hoops.

Cash management accounts are available across a variety of sources, including:

- Robo-advisers,

- online brokerages

- digital-only banks.

For example, robo-advisers like Syfe offer cash management accounts as a fuss-free way to grow cash holdings.

Meanwhile, some online brokerages such as Tiger Brokers and Moo Moo may offer in-house cash management accounts for traders to potentially enjoy better returns on their idle cash as they wait for market opportunities.

Maribank, a new-gen digital-only bank, also offers cash management via its MariInvest product.

Similarly, TrustInvest has a cash management account available under its Cash+ investment product.

What do cash management accounts invest in? Are they safe?

Typically, cash management accounts invest in a mix of money market funds and short-term investment-grade debt instruments.

These are generally considered lower risk investments on the market, which minimises potential risk to cash management account users.

The actual mix of funds, debt and cash instruments chosen varies among different cash management accounts. It’s advisable to check with your chosen provider for the exact money market funds in which your cash will be invested so you can have a clear idea of your risk exposure.

Chocolate Finance keeps risk low by diversifying across multiple funds. As at the time of writing, these are the funds included in the Chocolate managed account portfolio:

- Dimensional Short-Term Investment Grade Fixed Income SGD Fund (DSF)

- UOBAM United SGD Fund (USF)

- Fullerton Short Term interest rate SGD Fund (FST)

- LionGlobal Short Duration Bond SGD Fund (LGF)

- Amova Short Term Bond Fund (NST)

Note that these fund allocations may change at the discretion of the Investment team led by Benjamin Tan, Chief Investment Officer at Chocolate Finance. Adjustments made are in the service of optimising risk-adjusted returns based on factors like duration, yield to maturity, credit quality and currency.

These funds are invested globally to further optimise returns and diversify risks. But to protect against forex risk, investments in global currencies are hedged back to SGD.

Pro-tip: The Top-Up Programme – exclusive to Chocolate Finance – supports the returns on your first $50k in SGD and first $50k in USD. This means, if for some reason, the portfolio underperforms, the difference will be topped up to the stipulated returns, as follows:

Do note that the Chocolate Top-Up Programme is available during the Qualifying Period only.

The Qualifying Period runs from now until 30th June 2026, or until the assets under management for the Chocolate Managed Account reach S$1.5 billion – whichever comes first.

Chocolate Finance may, at its discretion, choose to extend or remove the Top-Up Programme.

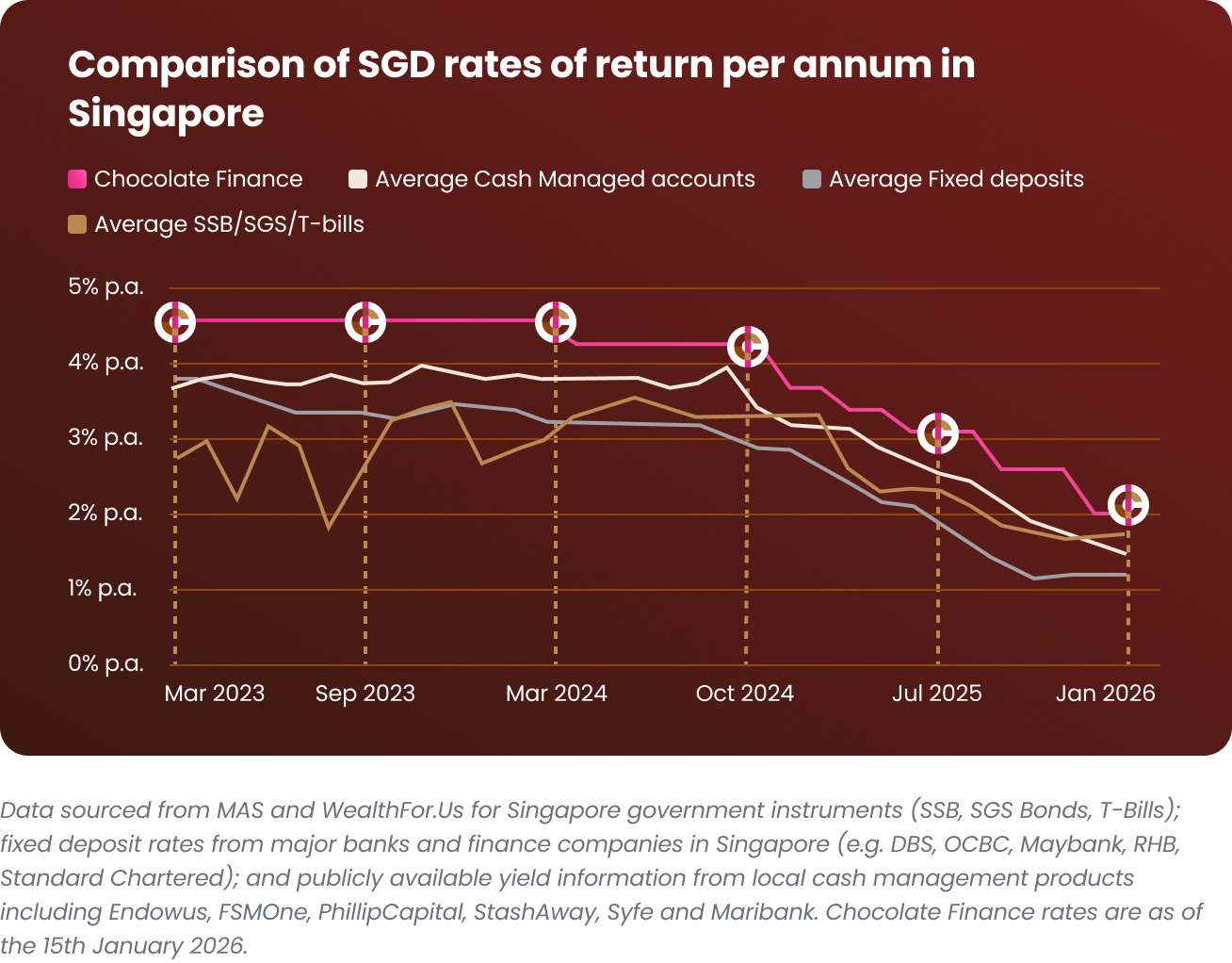

Cash management accounts vs bank savings accounts: returns compared

We’ll let the numbers speak for themselves. As you can see, this chart shows that Chocolate Finance consistently provides happy returns for a S$20,000 balance across an average of different savings/investment options available in Singapore as of January 2026.

Why Chocolate Finance is a unique Cash Management Account

You’ll find many cash management accounts on the retail market. Several are offered by online trading platforms as a means for investors to generate returns on cash balances in between trading opportunities.

Chocolate Finance is designed for everyone who wants to optimise returns on their cash, transparently and conveniently.

Daily returns tracking

Speaking of transparent, did you know that Chocolate lets you earn returns daily, which you can check at anytime on the app. There’s no need to wait till the end of the month to see returns added to your balance.

Flexible top-ups and withdrawals

And as for convenience, Chocolate offers instant top ups for your funds, and you can withdraw at any time – no lock-in, no minimum sums. Simply link your bank account to the Chocolate app to get started.

SGD and USD balances

Eyeing forex opportunities? You can choose between SGD and USD balance to diversify your funds. Chocolate offers hassle-free conversion between both currencies right on the app, so you can do everything you need in one go.

Visa debit card rewards

Finally, Chocolate comes with a VISA Debit Card that earns you 1 HeyMax mile per S$1 – capped at S$1,000 every month. Yes, Chocolate rewards you not only for saving, but also gives you more when it comes time to spend. I don’t think there’s any other cash management that does that.

Final thoughts: Is a Cash Management Account right for you?

Cash management accounts can be a smart way to earn better returns on spare cash in Singapore, especially if you want flexibility and don’t want to deal with bank bonus interest requirements.

Chocolate Finance offers a simple, transparent experience with supported returns (during the qualifying period), daily return visibili

Think Chocolate is right for you?

FAQs

Are cash management accounts safe in Singapore?

They typically invest in lower-risk instruments like money market funds and short-duration bonds, but they are still investment products and can carry risk.

Are cash management accounts SDIC-insured?

No - SDIC coverage generally applies to eligible Singapore dollar bank deposits, not investment products.

Can I withdraw money anytime from a cash management account?

Most cash management accounts allow withdrawals anytime, though processing times may vary by provider.

Are cash management accounts better than fixed deposits?

Cash management accounts are usually more flexible (no lock-in), while fixed deposits may offer guaranteed rates for a fixed tenure.

Disclaimer:

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)