Short-term savings is the foundation to breaking the paycheck-to-paycheck cycle. Here are five things to watch out for when managing your cash. It’s a few days to payday but your bank account is already empty. Bills are creeping nearer with each passing day, your cousin’s wedding is next week, and your insurer just sent you a reminder that your premiums are due next month… it never ends!

If the above sounds familiar to you, that’s because you’re probably one of the 40% of Singaporeans who live paycheck-to-paycheck. This is a stress-inducing situation; you’re always just a missed bill or unplanned expense away from permanently falling behind, which means you’re forced to keep a constant watch over your money, never able to fully relax.

But the good news is, like all vicious cycles, living paycheck-to-paycheck can be stopped. The key lies in realising that instead of spending your money willy-nilly, you need to plan your purchases, only buying what you want after you’ve saved up for it.

That’s right, breaking the paycheck-to-paycheck cycle is all about managing your short-term savings. As you get better at it, you’ll spend less time worrying about money, and more time enjoying what money can bring you. Now, isn’t that a worthy goal?

5 mistakes to avoid when managing your short-term savings

Successfully managing short-term savings hinges on making the right choices while avoiding the wrong ones. If you want to steer clear of common mistakes, it's important to understand the impact of each decision you make. Here are five mistakes to watch out for that could sabotage your short-term savings.

Not automating your savings

Trying to save on willpower alone isn’t likely to get you very far. To make it a long-term habit, try automating your savings instead. This means automatically depositing a portion of your salary into your savings account, only leaving the remainder for your expenses.

Automating your savings makes it so that you save first, and spend the rest, instead of spending first and attempting to save what’s leftover at the end of the month.

Singapore’s MoneySense initiative recommends saving 20% of your monthly income automatically before spending anything else, a habit proven to improve financial security.

Handily, automating your savings dramatically increases your chances of success.

“Studies have shown that if you automate savings, the chance of success and the savings rate increases by 70%,” shared Benjamin Tan, CIO, Chocolate Finance during a guest appearance on Money Hacks, a personal finance podcast by Business Times on 3rd November 2025.

Benjamin explained that this is a simple habit that is not complicated nor flashy, but it quietly compounds its benefits over time.

Not watching your money leaks

No matter how adept you are at earning money, money leaks can leave you constantly feeling unable to keep up with your expenses.

Recent surveys show that nearly 27% of Singaporeans in their 20s admit to spending beyond their means to keep up with peers, with online shopping, food delivery and lifestyle spending cited as top culprits.

A money leak refers to an avoidable situation which causes you to spend more money than necessary. “The key idea is to avoid wealth erosion or wealth leakages,” stated Benjamin.

One common example of a money leak is not clearing your credit card bills. You may think that it’s ok to carry a balance on your credit card, and regard the monthly finance charge (i.e., interest) as a small price to pay for the convenience of spending as you please.

While the finance charge you see on your monthly statement may appear to be a relatively small amount, such charges add up. On average, credit cards in Singapore charge interest of approximately 28% to 30% per annum on overdue amounts – making them one of the most expensive ways to spend on unsecured credit.

If you’re not diligently paying off your credit card bills in full every month, you’re simply letting money leak out of your grasp. To keep the money in your account and grow your short term savings, it’s crucial to avoid unnecessary expenses that cause these leaks. Other money leaks to watch for include unused memberships and subscriptions, excessive use of food delivery (prices in-app are often higher than dining in), and buying things or subscribing to services that you don’t actually need.

Not having a framework

Applying a framework to your spending can be valuable in managing your short-term savings. Benjamin recommends using a 40-30-20-10 framework, where “40% of your income goes to meeting needs – lodging, transportation, utilities, food”.

“30% is for savings. It may sound like it’s a lot, but remember that 20% of your salary goes to CPF. So this means you need only save another 10% of your income for savings and investments,” he explained.

Meanwhile Benjamin suggests that 20% of our income can be used for discretionary spending, such as for leisure, travel or hobbies. As for the remaining 10%, Benjamin points out that we should use this amount to upskill ourselves, learn new capabilities and improve our standing in the jobs market.

You can finetune the framework to suit your personal circumstances and choose the right allocation for you based on your unique situation. Still living with your folks? Allocate a larger percentage to savings and investments. Need to provide for your growing family? Reduce your discretionary spending and self-education buckets by 5% each.

Not gamifying your goals

Another interesting observation that was discussed during the podcast was how only one-third of Gen Z was confident in managing their money. The implication here is that the larger majority of young Singaporeans were unsure how to exercise this critical life skill.

“Confidence comes with control,” observes Benjamin, who recommends savers start by gaining awareness of their money flows with the use of budget tracking apps. Then, to build confidence, savers should start small and let the habit build over time. “The habit (of regularly setting money aside) builds confidence. The earlier they see the progress, the faster they’ll feel in control of their financial future,” he added.

Beside educating yourself on personal finance, another way to improve your success at managing your savings is to gamify your goals. This turns what can be a repetitive task into a more entertaining experience, motivating you to keep going. The best gamification strategies for building savings habits include using progress tracking, setting milestone rewards, and creating friendly competitions, which can significantly boost motivation and consistency.

This is especially useful for younger savers, over two-thirds of Gen Z Singaporeans feel uncertain about managing money, often due to a lack of early financial wins. Gamified tools help bridge this gap.

Think how language-app Duolingo leverages learning streaks to encourage users to keep up with their lessons. Try applying a similar tactic to your own savings goals, perhaps sharing your saving streaks with your friends or by starting an interest group via WhatsApp, Telegram or social media, or challenging family members to a leaderboard.

Not rebranding your retirement

The habits that help you get out of living paycheck-to-paycheck can also be applied to longer-term financial goals, such as planning for your retirement. In fact, it is important to plan for long term financial security to ensure stability and peace of mind in the future. This is another major financial roadblock that plagues many Singaporeans.

When you’re in your 20s or 30s and retirement is literal decades away, it can be tempting to put off planning for it until later. After all, there are so many other important and more immediate goals to work on first, right?

Benjamin acknowledges that retirement can be a difficult subject to approach, “Oh, (retirement) is a distant goal. It’s daunting, and therefore, let’s give up, let’s YOLO.” To counter this negative mindset, he suggests reframing what retirement means to you. “Why not just invest or subscribe to your future self? It’s just like paying for video streaming or subscription – you automate your savings, just set it aside in a retirement or savings pot.”

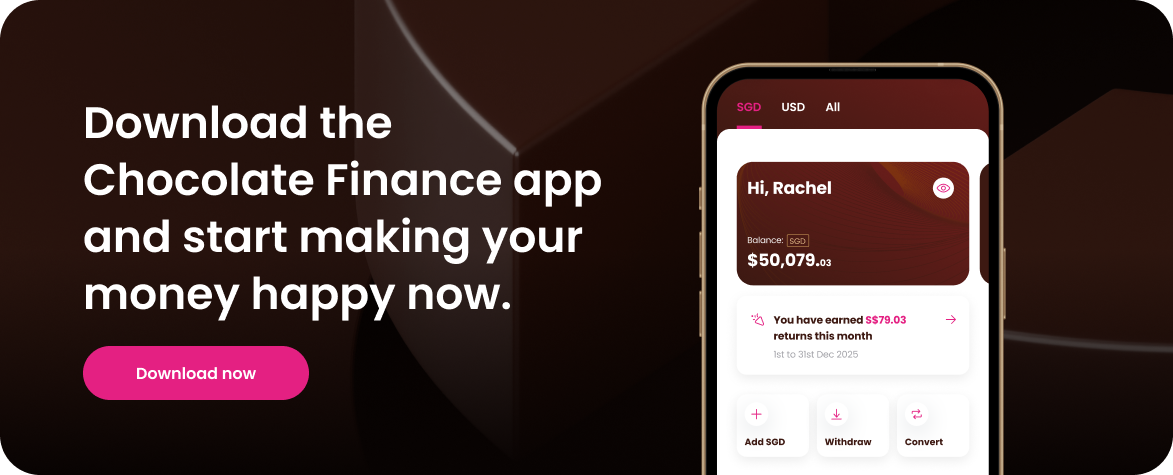

How Chocolate Finance helps you stop living from paycheck-to-paycheck

It’s easy to start (and keep) saving money with instant deposit

Chocolate makes it easy to start saving with our mobile app. Make instant deposits using PayNow – it literally takes just seconds for your funds to be transferred.

Gamify your goals with daily returns

Stay on track with the easiest, most satisfying winning streak ever! Earn returns on your balances daily which you can see right on the app. No second-guessing, no waiting for monthly statements, just complete transparency so you can check on your progress all day, everyday.

Accelerate your goals with happy returns

With Chocolate, your money goals get a boost so you can accelerate your progress.

Starting 1 Dec 2025, your SGD balance will earn up to 2% p.a., while USD balances earn up to 4.1% p.a. Here’re the details:

Stretch your dollar with HeyMax Miles

Chocolate makes spending more rewarding. You can earn HeyMax Miles when you spend with the Chocolate Visa Debit card at the rate of 1 mile per dollar (for the first S$1,000 spent per month), and 0.4 miles per dollar thereafter. Use HeyMax miles for flight tickets, hotel bookings, or to purchase gift cards.

And speaking of travelling, did you know the Chocolate Visa Debit Card also lets you enjoy zero FX fees when spending in foreign currencies? Yep, Chocolate makes happy money even happier!

Break the cycle with Chocolate

Clearly, living paycheck to paycheck is less than ideal and we should all aim to stop this vicious cycle before things get any worse. Getting out of living paycheck-to-paycheck is far from an impossible task, but you do need to build useful habits such as paying attention to how you manage your short-term savings, as well as adapt your mindset around long-term goals such as planning for retirement.

By starting small, automating your savings, and using gamification to stay motivated, you’ll better build the foundational habits that will reward you with better control over your financial future.

Ready to break free from the stress and anxiety of living paycheck to paycheck? Sign up for Chocolate now.

Disclaimer:

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)