You've probably seen both terms floating around — on bank posters, in finance apps, across comparison sites. They can look interchangeable. They're not. And understanding the difference could change how you think about where you keep your money.

We often get customers asking for “what is Chocolate Finance interest rate” and we always respond:

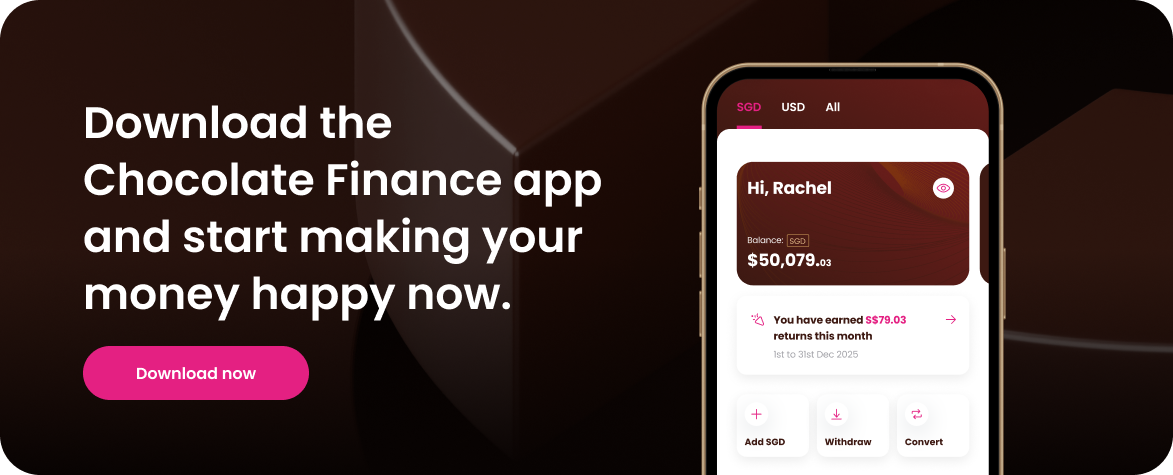

Chocolate Finance offers a return of 2% p.a. on your first S$20k, 1.8% p.a. on your next S$80k, and up to 1.8% p.a. on any amount thereafter. Daily returns. No lock-ins. No complex criteria or hoops to jump through.

See your returns daily in the app - if we don't make the returns for your first S$100k or US$100k, the difference will be topped up during the Qualifying Period. Learn more about the Top-Up Programme.

With the Chocolate USD account, enjoy 4.1% p.a. on your first US$20k, 3.8% on your next US$80k, and up to 3.8% p.a. on balances above US$100k.

Note: Chocolate Finance is not a bank and doesn't 'offer interest'. Instead, your money earns a 'return' based on the performance of the Chocolate Managed Account portfolio designed to deliver the return.

So let us help you understand the difference:

What is an interest rate?

An interest rate is what a bank or financial institution promises to pay you for keeping your money with them. It's a fixed, pre-set percentage — often annualised — that gets calculated on your balance and paid out on a schedule.

The key word here is promised. A traditional savings account interest rate is contractual. The bank tells you upfront: "Keep your money here, and we'll pay you X% per year." Full stop.

That sounds great. And it can be. But there are a few things worth knowing:

- Interest rates on savings accounts are often set low — sometimes well below inflation

- The rate can change, especially on variable-rate accounts, and banks don't always shout about it when it drops

- You're usually earning interest that goes straight back into the same account, which means your money isn't doing much work beyond sitting there

It can look like this DBS example:

Fixed interest vs variable interest

When banks talk about a fixed interest rate, they mean the rate is locked for a defined period — say, three, six or twelve months. After that, you're usually moved onto a lower standard rate unless you actively switch. Variable rates, by contrast, move with market conditions which can work in your favour, but just as easily work against you.

Competitive interest rates and the small print

Banks often advertise a competitive interest rate to draw you in. But "competitive" is doing a lot of heavy lifting in that sentence. Look closer and you'll often find the headline rate is a bonus interest rate — an elevated figure that only applies when you meet a set of conditions. Credit a salary each month. Make a minimum number of transactions. Maintain a specific balance tier. Miss one condition, and that attractive rate disappears.

This is how a "competitive" rate of 3% or 4% can quietly become 0.05% if your behaviour doesn't tick all the boxes. The interest is real — the accessibility of it often isn't.

What is a returns rate?

A returns rate — or simply, your returns — is the actual performance of your money over time. Rather than being a single fixed promise, it reflects what your balance genuinely earns based on where and how that money is being used.

Returns can come from multiple sources: yields on financial instruments, income generated by portfolios, and the compounding effect of reinvesting what you earn ( ie your returns also earn returns). The result is a number that more accurately reflects what your money is doing in the real world.

This is why you'll see us talk about returns at Chocolate Finance, rather than interest. When you add money to your Chocolate Finance account, it's not just sitting in a vault earning a token percentage. It's working — and your returns reflect that.

Why does the distinction matter?

Here's the practical bit.

When a bank advertises an interest rate, they're telling you about a product they've designed. When a returns rate is quoted, it reflects actual performance — what the money earned over a given period.

The difference matters because:

Interest rates might not always be what they seem. A headline rate of 3% might come with conditions — minimum balances, lock-in periods, need to add your salary each month, or an introductory window that will expire after a few months. Read the small print and the number often gets smaller. People often refer to the “realistic rate” which is what most people actually achieve.

Whereas when returns are based on actual portfolio performance, there's less room to hide behind asterisks. What you see is closer to what you get.

Your money deserves to work harder. Traditional fixed interest lacks growth potential beyond its fixed yield. Returns — particularly when generated from a diversified approach — have the potential to compound and grow in ways that a fixed rate simply can't replicate.

How the Chocolate Finance top up programme works

One of the things we're proud of at Chocolate Finance is how we've made growing your balance genuinely simple.

The Top-Up Programme is a promotional incentive. It's been put in place to support the returns on your first S$100k (currently 2% p.a. on your first S$20k and 1.8% p.a. on your next S$80k) and your first US$100k (currently 4.1% p.a. on your first US$20k and 3.8% p.a. on your next US$80k) during the Qualifying Period. This means, if for some reason, the portfolio underperforms, the difference will be topped up so you enjoy the current rate.

This stands in contrast to how bonus interest rate structures typically work at traditional banks, where you often have to do several things simultaneously just to access the rate that was advertised to you. With Chocolate Finance, the rate you see is the rate your money earns. That's it.

So which is better?

Neither term is inherently better — what matters is understanding what's behind the number.

A high interest rate with a short introductory period and strict conditions might feel good on paper but underperform in practice. A returns rate that's grounded in real portfolio activity, with no lock-ins and full flexibility, can make a meaningful difference to your balance over time.

The bottom line

Interest rate = what a bank promises to pay you, often with conditions attached.

Returns rate = what your money actually earns based on real activity.

The gap between those two things is often where the real opportunity lies. Whether you're comparing fixed interest accounts, chasing a competitive interest rate, or trying to figure out if a bonus interest rate is actually worth it — now you know what to look for.

Disclaimer

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Download the app and sign up now.

It only takes a few minutes.

.webp)

.jpg)

.png)