We all have cash sitting idle — whether it’s for an emergency fund or the next holiday — and now is a great time to think about how to make that money work harder for you. Whether you’re saving for short-term goals or looking to earn a little extra on the side, understanding your options is key.

In this market overview, we’ll break down the best lower risk investment options outside of traditional bank savings accounts for your spare cash in Singapore right now — from fixed deposits to Singapore Savings Bonds and everything in between.

Aside from traditional savings accounts, which often come with complicated criteria and fine print, here are some of the best options for your cash in Singapore in 2025:

1. Fixed deposits

Fixed deposits (FDs) are a popular choice for savers seeking stable returns. These accounts typically offer lower rates compared to more dynamic investments but come with the benefit of being SDIC-protected (up to S$100,000 per depositor per bank), ensuring the safety of your money even if the bank encounters issues.

Fixed deposits are ideal if you don’t need immediate access to your funds and want to secure a predictable return over a set period.

Read more about fixed deposits

2. Cash Managed Accounts

Cash-managed accounts are becoming increasingly popular for those looking to earn better returns than traditional savings accounts while still maintaining relatively high liquidity.

These accounts typically invest in short-duration, investment-grade bonds, meaning you may experience fluctuations in returns, but the risk is usually low. They're a good middle ground between fixed deposits and more volatile investments.

3. Treasury Bills (T-Bills)

Issued by the Monetary Authority of Singapore (MAS) which is backed by the Singapore government, T-bills are one of the safest ways to park your money. These short-term securities typically mature in 6 months or 1 year and offer a guaranteed return backed by the government.

While T-bills are a very low-risk option, they don’t always offer the highest yields compared to other investment vehicles. However, they provide peace of mind with the government’s backing.

Read more about treasury bills

4. Singapore Savings Bonds (SSBs)

Singapore Savings Bonds are another government-backed option. These bonds offer a guaranteed return that increases over a 10-year period.

While the yield in the first year is modest, it gradually improves over time, making SSBs a good option for long-term savers. There are limits on the amount you can invest, but they remain a low-risk, stable option for individuals looking for steady, government-backed growth.

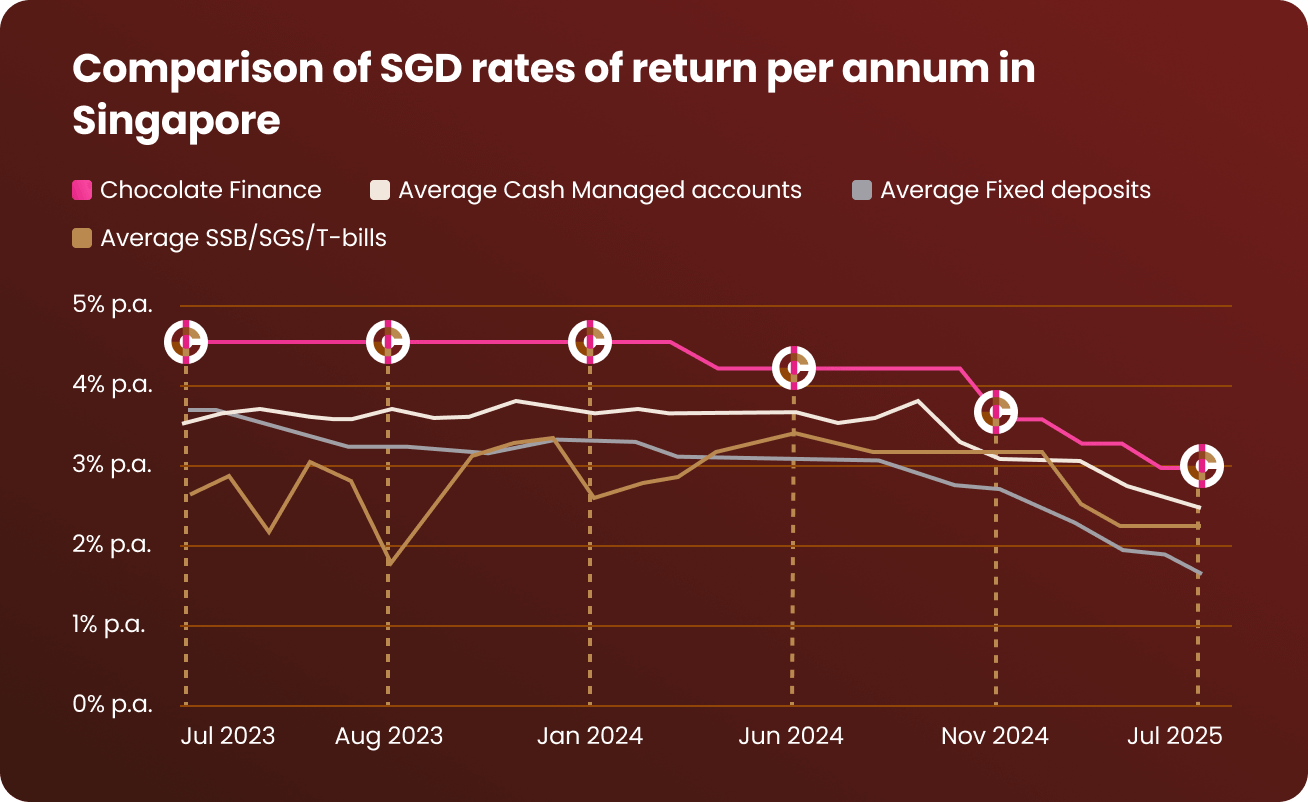

Best places for your spare cash in Singapore

Here’s a side-by-side comparison of the best returns for a S$20,000 balance across different savings/investment options available in Singapore as of June 2025.

Product |

Provider |

Yield (% p.a.) |

Minimum deposit |

Criteria to earn rate |

Restrictions |

|---|---|---|---|---|---|

Cash-Managed Account - Low Risk |

2.5% |

N/A |

No criteria, no minimums no maximums. |

Not guaranteed - although the top-up programme is only available during the Qualifying Period. No lock-ins. |

|

Cash-Managed Account - Low Risk |

2.5%* |

N/A |

- |

The projected rate is not guaranteed and is 2.5%* p.a. as of 18 Jul 2025. T&Cs apply. |

|

Best Fixed Deposit (12-month) |

1.6% |

$1,000 |

Minimum investment of $1,000 |

Maximum investment of $19,999 |

|

Singapore Savings Bonds (SSB) |

1.56% |

$500 |

The minimum amount for investing in Singapore Savings Bonds (SSBs) is S$500. Additional investments can be made in multiples of S$500, up to a maximum of S$200,000 per investor. |

First yr 1.56%. If you hold the SSB for 10 years, you will receive an average interest rate of 1.93% per annum. Closing date: 25th September 2025 • Issue date: 1st October 2025. |

|

Treasury Bills (T-Bills) |

1.44% |

$1,000 |

The minimum bid amount is S$1,000, and subsequent investments must be in multiples of S$1,000. |

The cut off yield for the 6-month Singapore T-bill (BS25117E) fell to 1.44% in the auction on 28 August 2025. |

|

Best Fixed Deposit (6-month) |

1.4% |

$1,000 |

Minimum investment of $1,000 |

Maximum investment of $19,999 |

|

Best Fixed Deposit (3-month) |

1.4% |

- |

- |

Promotional rates are subject to change without prior notice. Terms and conditions apply. |

Product |

Provider |

Yield (% p.a.) |

Minimum deposit |

Criteria to earn rate |

Restrictions |

|---|---|---|---|---|---|

Cash-Managed Account - Low Risk |

3% |

N/A |

No criteria, no minimums no maximums. |

Not guaranteed - although the top-up programme is only available during the Qualifying Period. No lock-ins. |

|

Cash-Managed Account - Low Risk |

2.4% - 2.5% |

N/A |

No lock ins, no minimum balance |

Cash+ Flexi projected returns are based on annualised amortised yield estimates of the underlying funds provided by the fund managers, as of 30 June 2025 14:30 SGT |

|

Best Fixed Deposit (12-month) |

2.45% |

$1,000 |

Minimum investment of $1,000 |

Maximum investment of $19,999 |

|

Best Fixed Deposit (6-month) |

2.15% |

$1,000 |

Minimum investment of $1,000 |

Maximum investment of $19,999 |

|

Treasury Bills (T-Bills) |

1.77% |

$1,000 |

The minimum bid amount is S$1,000, and subsequent investments must be in multiples of S$1,000. |

The cut off yield on the 6-month Singapore T-bill was at 1.77% on 31 July 2025. |

|

Singapore Savings Bonds (SSB) |

1.71% |

$500 |

The minimum amount for investing in Singapore Savings Bonds (SSBs) is S$500. Additional investments can be made in multiples of S$500, up to a maximum of S$200,000 per investor. |

First yr 1.71%. If you hold the SSB for 10 years, you will receive an average interest rate of 2.11% per annum. Closing date: 26th August 2025 • Issue date: 1st September 2025. |

|

Best Fixed Deposit (3-month) |

1.7% |

$500 |

Minimum investment of $500 |

Mobile banking promo rates for new placement only |

Which option is best for your cash?

There are plenty of options available in the market for your cash, but what you choose depends on your needs.

- If you want stability and low risk, and are not worried about lock in periods – fixed deposits or T-bills might be a great fit.

- On the other hand, if you’re looking for higher yields without locking up your funds for too long, cash-managed accounts or Singapore Savings Bonds could be better options.

Ultimately, there’s no one-size-fits-all solution. Each option has its pros and cons, so it’s essential to evaluate your financial goals and your tolerance for risk before deciding where to park your cash.

Whatever you choose, make sure it aligns with your financial plans and provides you with the best return for your money in 2025.

Looking at higher returns alongside liquidity

In ‘Tim Phillips’ words’

If you’re an investor who wants to get a yield on your cash, the options out there aren’t exactly plentiful. We’ve seen yields on 6-month Singapore T-bills hit multi-year lows (of below 1.4%) and Singapore Savings Bonds (SSBs) also offering up yields not much higher.

Why? Mainly down to expectations that the US Federal Reserve (Fed) will be cutting rates again, starting at its 16-17 September meeting. That has resulted in lower yields in Singapore too.

However, one of the more attractive yields on offer is the Chocolate Finance SGD Managed Account that offer 2.5% p.a. On the first $20k and then up to 2.2% p.a. for the next $30k. While investors should remember that the yield is generated from a selection of investment-grade, short-duration bonds funds, the risk profile of the offering is still extremely low risk. Finally, it also offers investors flexibility in terms of being able to withdraw quickly – making it an ideal place to earn a yield on your emergency funds.

Source: Chocolate Finance SGD Cash Managed Account, 15th September 2025

We think your spare cash deserves better

In the world of financial products, many options come with complex rules, hidden fees, or long lock-in periods. But with Chocolate Finance, you get happy returns, flexibility, and transparency — without any unnecessary restrictions.

So, whether you’re parking your emergency fund or looking for a better way to grow your spare cash, Chocolate Finance works hard to make the most of your money for you. No complicated terms, no minimums, and most importantly, no waiting around for your cash to grow - see your returns every single day.

It's time to stop leaving money on the table and start making your spare cash work harder for you. With Chocolate Finance, your spare cash is in good hands.

Disclaimer:

Chocolate Finance is a brand of Chocfin Pte Ltd and is regulated by the Monetary Authority of Singapore. The views and opinions expressed on this post are solely those of the original authors and contributors as of the date of this post and are subject to change based on market and other conditions. This is for information only and does not constitute an offer or solicitation to buy or sell any of the investments mentioned. Neither Chocfin Pte. Ltd. (“Chocfin”) nor any officer or employee of Chocfin accepts any liability whatsoever for any loss arising from any use of this blog or its contents.

Please note that Chocfin does not guarantee the accuracy, relevance, timeliness, or completeness of the information provided on this post. The inclusion of any links does not necessarily imply a recommendation or endorse the views expressed within them. Chocolate’s returns are currently supported by a promotional 'Top-Up Programme', valid during the Qualifying Period and subject to terms and conditions. Past performance is not indicative of future results. All investments involve risk, including the risk of losing all of the invested amount and may not be suitable for everyone. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Related articles

Download the app and sign up now.

It only takes a few minutes.

.jpg)

.png)